Third Straight Month

According to a recent Reuters poll , investors are increasingly bullish

on emerging market Asian

currencies, including

the Taiwan dollar,

Indonesian rupiah,

Singapore dollar,

Malaysian ringgit,

Philippine peso, South

Korean won, and Indian

rupee. The Thai Baht

wasn’t covered by the

poll, but given its

strong performance over

the last few months, it

seems safe to include it

in the bunch.

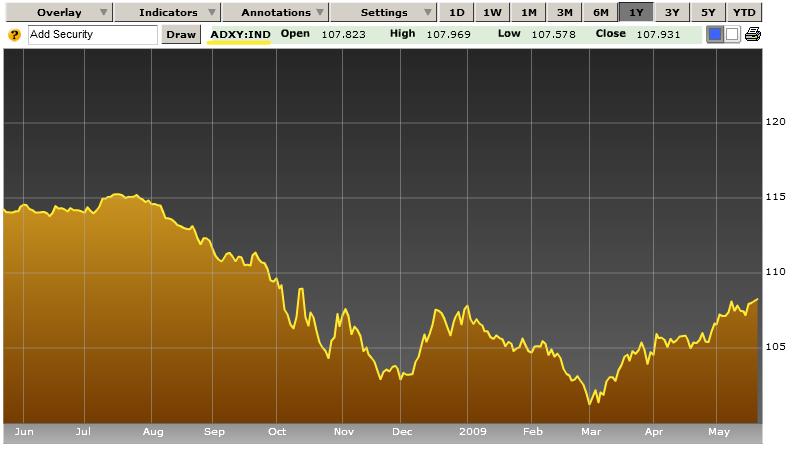

This uptick in sentiment is somewhat unspectacular, since “The

Bloomberg-JPMorgan Asia

Dollar Index, which

tracks the 10

most-active regional

currencies,” has now

risen for almost three

consecutive months [See

chart below]. Leading

the pack are the Taiwan

Dollar and South Korean

Won, which recently

touched five-month and

seven-month highs,

respectively. “The

Korean currency has

climbed 28 percent since

reaching an 11-year low

of 1,597.45 in March.”

Investors are now pouring money back into Asia at rapid clip. “Asia

ex-Japan received $933

million in the week

ended May 20, the most

among emerging-market

stock funds, bringing

the total this year to

$6.9 billion .”

Meanwhile, the “The MSCI

Asia Pacific Index of

regional stocks climbed

22 percent this quarter”

while Chinese stocks are

up 45% since the

beginning of 2009.

But it’s unclear - doubtful is a

better word - whether

this rally is supported

by economic

fundamentals. One

commentator summarized

this contradiction as

follows: “Improved

sentiment has led to a

massive resurgence in

flows to emerging

markets, irrespective of

the underlying data,

which remains weak.

Investors are going out

of dollars to riskier

markets, riskier

currencies."

Let’s drill down into some of the data. Chinese exports fell 15% in

April. Japan’s economy

contracted 15% in the

most recent quarter.

Singapore’s exports are

down 20% on an

annualized basis. The

South Korean economy is

projected to shrink by

2% this year. The

Central Bank of Thailand

just cut its benchmark

interest rate to an

unbelievable 1%. The

only bright spot

economically is Taiwan,

which is benefiting both

from improved economic

ties with China and a

healthy current account

surplus. I suppose

everything is relative,

as “developing Asian

economies will

grow 4.8 percent in

2009, even as the world

economy contracts 1.3

percent” according to

the International

Monetary Fund.

The notion that the rally is not rooted in fundamentals is shared by

the region’s Central

Banks, which clearly

realize that economic

recovery will be much

more difficult in the

face of currency

appreciation. One

analyst argues that,

“Until the signs of

global economic recovery

become more convincing,

central banks will

unlikely tolerate

significant currency

appreciation." The

Central Banks of South

Korea, Taiwan, and

Indonesia have already

actively intervened to

hold their currencies

down, while Malaysia and

Singapore (discussed in

a

Forexblog post last

week) have also

intervened for the sake

of stability.

As a result, this rally could soon begin to lose steam. “A ‘correction’

in regional currencies

is ‘appropriate’

following recent gains,”

said one analyst.

Another has called the

rally “overdone.” Still,

Central Banks and

economic data pale in

comparison to capital

flows and risk/reward

analysis. In short,

these currencies (and

other investments) will

continue to find buyers

for as long as there are

those hungry for risk.

Citigroup, whose “Asia-Pacific

foreign-exchange volume

may rise about 10

percent from the first

quarter,” is bullish. A

representative of the

firm declared: “Fund

managers are still

’sitting on lots and

lots of cash’ so the

pickup in volumes will

continue.”

ليست هناك تعليقات:

إرسال تعليق